5.7 KiB

3.2.9 时间序列的高级应用

相关知识

Pandas 时间序列工具的基础是时间频率或偏移量代码。就像之前见过的D(day)和H(hour)代码,我们可以用这些代码设置任意需要的时间间隔。

Pandas频率代码表如下:

| 代码 | 描述 |

|---|---|

| D | 天(calendar day,按日历算,含双休日) |

| W | 周(weekly) M 月末(month end) |

| Q | 季末(quarter end) |

| A | 年末(year end) |

| H | 小时(hours) |

| T | 分钟(minutes) |

| S | 秒(seconds) |

| L | 毫秒(milliseonds) |

| U | 微秒(microseconds) |

| N | 纳秒(nanoseconds) |

| B | 天(business day,仅含工作日) |

| BM | 月末(business month end,仅含工作日) |

| BQ | 季末(business quarter end,仅含工作日) |

| BA | 年末(business year end,仅含工作日) |

| BH | 小时(business hours,工作时间) |

| MS | 月初(month start) |

| BMS | 月初(business month start,仅含工作日) |

| QS | 季初(quarter start) |

| BQS | 季初(business quarter start,仅含工作日) |

| AS | 年初(year start) |

| BAS | 年初(business year start,仅含工作日) |

时间频率与偏移量

我们可以在频率代码后面加三位月份缩写字母来改变季、年频率的开始时间,也可以再后面加三位星期缩写字母来改变一周的开始时间:

Q-JAN、BQ-FEB、QS-MAR、BQS-APR等W-SUN、W-MON、W-TUE、W-WED等

时间频率组合使用:

In[0]:pd.timedelta_range(0,periods=9,freq="2H30T")

Out[0]:TimedeltaIndex(['00:00:00', '02:30:00', '05:00:00', '07:30:00', '10:00:00', '12:30:00', '15:00:00', '17:30:00', '20:00:00'], dtype='timedelta64[ns]', freq='150T')

比如直接创建一个工作日偏移序列:

In[1]:from pandas.tseries.offsets import BDay

pd.date_range('2015-07-01', periods=5, freq=BDay())

Out[1]:DatetimeIndex(['2015-07-01', '2015-07-02', '2015-07-03', '2015-07-06', '2015-07-07'], dtype='datetime64[ns]', freq='B')

重新取样、迁移和窗口

重新取样

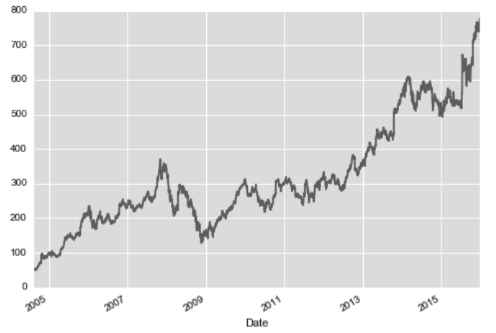

处理时间序列数据时,经常需要按照新的频率(更高频率、更低频率)对数据进行重新取样。举个例子,首先通过pandas—datareader程序包(需要手动安装)导入 Google 的历史股票价格,只获取它的收盘价:

In[2]:

from pandas_datareader import data

goog = data.DataReader('GOOG',start="2014",end="2016",data_source="google")['Close'] # Close表示收盘价的列

In[3]:

import matplotlib.pyplot as plt

import seaborn; seaborn.set()

goog.plot(); #数据可视化

输出:

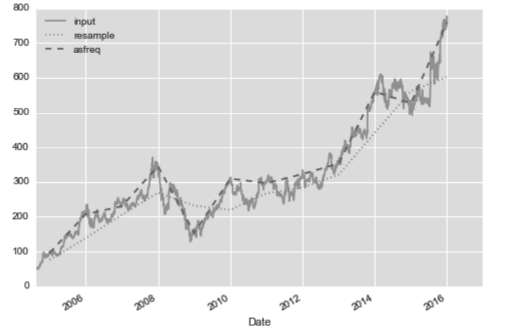

我们可以通过resample()方法和asfreq()方法解决这个问题,resample() 方法是以数据累计为基础,而asfreq()方法是以数据选择为基础。

In[4]:

goog.plot(alpha=0.5, style='-')

goog.resample('BA').mean().plot(style=':')

goog.asfreq('BA').plot(style='--');

plt.legend(['input', 'resample', 'asfreq'], loc='upper left');

输出:

请注意这两种取样方法的差异:在每个数据点上,resample反映的是上一年的均值,而asfreq反映的是上一年最后一个工作日的收盘价。

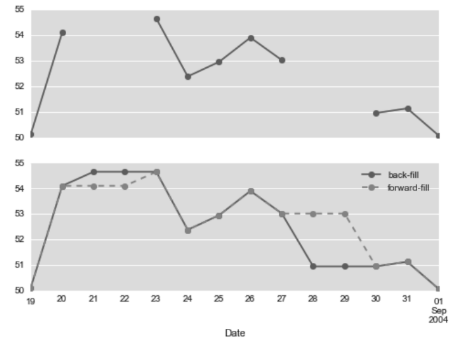

数据集中经常会出现缺失值,从上面的例子来看,由于周末和节假日股市休市,周末和节假日就会产生缺失值,上面介绍的两种方法默认使用的是向前取样作为缺失值处理。与前面介绍过的pd.fillna()函数类似,asfreq()有一个method参数可以设置填充缺失值的方式。

In[5]:fig, ax = plt.subplots(2, sharex=True)

data = goog.iloc[:10]

data.asfreq('D').plot(ax=ax[0], marker='o')

data.asfreq('D', method='bfill').plot(ax=ax[1], style='-o')

data.asfreq('D', method='ffill').plot(ax=ax[1], style='--o')

ax[1].legend(["back-fill", "forward-fill"]);

输出:

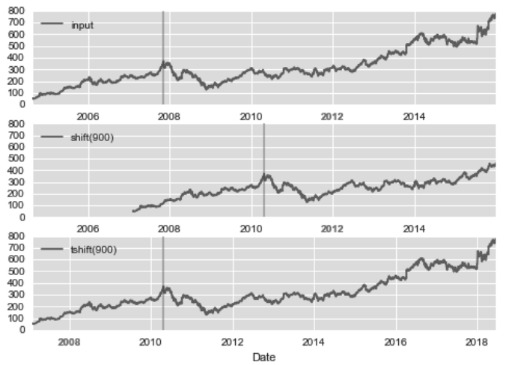

时间迁移

另一种常用的时间序列操作是对数据按时间进行迁移,Pandas有两种解决这类问题的方法:shift()和tshift()。简单来说,shift()就是迁移数据,而 tshift()就是迁移索引。两种方法都是按照频率代码进行迁移。

下面我们将用shift() 和tshift()这两种方法让数据迁移900天:

In[6]:fig, ax = plt.subplots(3, sharey=True)

# 对数据应用时间频率,用向后填充解决缺失值

goog = goog.asfreq('D', method='pad')

goog.plot(ax=ax[0])

goog.shift(900).plot(ax=ax[1])

goog.tshift(900).plot(ax=ax[2])

# 设置图例与标签

local_max = pd.to_datetime('2007-11-05')

offset = pd.Timedelta(900, 'D')

ax[0].legend(['input'], loc=2)

ax[0].get_xticklabels()[4].set(weight='heavy', color='red')

ax[0].axvline(local_max, alpha=0.3, color='red')

ax[1].legend(['shift(900)'], loc=2)

ax[1].get_xticklabels()[4].set(weight='heavy', color='red')

ax[1].axvline(local_max + offset, alpha=0.3, color='red')

ax[2].legend(['tshift(900)'], loc=2)

ax[2].get_xticklabels()[1].set(weight='heavy', color='red')

ax[2].axvline(local_max + offset, alpha=0.3, color='red');

输出:

shift(900)将数据向前推进了900天,这样图形中的一段就消失了(最左侧就变成了缺失值),而tshift(900)方法是将时间索引值向前推进了900天。

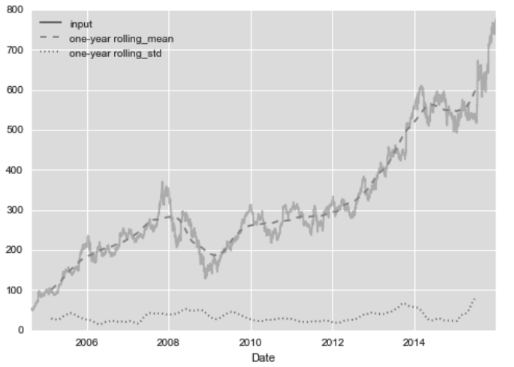

移动时间窗口

Pandas处理时间序列数据的第3种操作是移动统计值。这些指标可以通过 Series和DataFrame的rolling()属性来实现,它会返回与groupby操作类似的结果,移动视图使得许多累计操作成为可能。

In[7]: rolling = goog.rolling(365, center=True)

data = pd.DataFrame({'input': goog, 'one-year rolling_mean': rolling.mean(), 'one-year rolling_std': rolling.std()})

ax = data.plot(style=['-', '--', ':'])

ax.lines[0].set_alpha(0.3)

输出: